Income Smoothing & The New $40,000 SALT Landscape

Income Smoothing & The New $40,000 SALT Landscape

Target Audience: High-net-worth individuals in high-tax states (CA, NY, NJ, etc.).

The Strategy

For years, the "SALT Cap" limited state and local tax deductions to a measly $10,000. In 2026, the game has changed. The SALT cap has been raised to $40,000 (phasing out for those making $500k+), and the standard deduction has nearly doubled.

Section 1202 – The $15 Million Tax-Free Exit

Section 1202 – The $15 Million Tax-Free Exit

Target Audience: Founders, early employees, and Angel investors.

The Strategy

Internal Revenue Code Section 1202, also known as Qualified Small Business Stock (QSBS), is arguably the most powerful tax break in existence. It allows you to exclude up to 100% of capital gains on the sale of stock in certain small businesses.

The "Mega Backdoor" – Moving $40k+ Into a Roth in 2026

The "Mega Backdoor" – Moving $40k+ Into a Roth in 2026

Target Audience: High-earning W-2 employees or Solo 401(k) owners.

The Strategy

While most taxpayers are limited to a $7,000 annual Roth IRA contribution (for those under 50), high earners often find themselves "phased out" by income limits. The Mega Backdoor Roth allows you to bypass these limits and contribute up to $47,500 additional into a tax-free Roth account in 2026.

The "60/40 Rule" is Dead: Why Your S Corp Salary Methodology Won't Survive an Audit

For years, many tax professionals relied on the "Sleep Well at Night" percentage. They would tell their S Corp clients: "Just take 60% as salary and 40% as distributions. The IRS won't bother you."

It was simple. It was easy. And it is completely legally baseless.

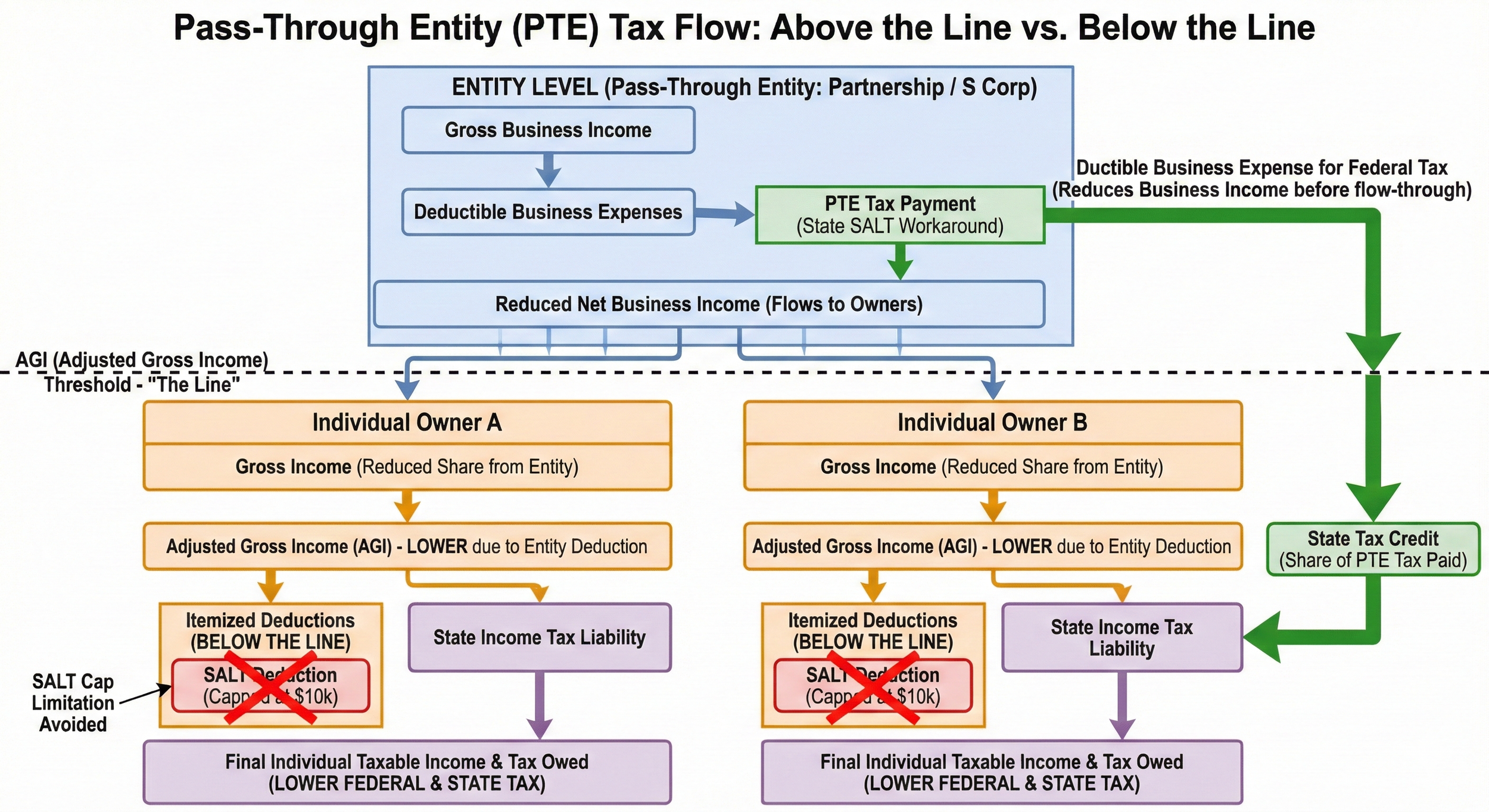

Beyond the SALT Cap: A Deep Dive into PTE Tax Mechanics, History, and Hidden Traps

We all know the basic pitch: "Pay the tax at the entity level to bypass the individual cap." But as we move past the initial rollout phase, the cracks in the pavement are starting to show. From the "Trade or Business" requirement to the timing of payments, the PTE election is not a one-size-fits-all deduction.

Here is a deep dive into the history, the mechanics, and the scenarios where this "perfect" loophole can actually backfire.

The “Mandatory” Step-Down: Why You Can’t Ignore Section 743(b) Just Because You Didn’t Check the Box

We all love a Step-Up. When a partner buys an interest and the assets have appreciated, we race to file a Section 754 Election to get that sweet extra depreciation.

But what happens when the assets have lost value?

The natural instinct is to be an ostrich: "Let's just NOT file the 754 election. No election, no step-down, no lost basis. Right?"

The $0 Liquidation Value: How to Grant Profits Interest Without Triggering a Tax Bill

Stop guessing on liquidation values. The Targeted Allocation Engine allows you to build custom distribution tiers with hurdle rates in minutes. Prove the $0 liquidation value, protect your client’s Safe Harbor, and standardize your partnership workpapers.

The “Doomsday Simulation”: Why Your Recourse Debt Allocations Might Fail under Audit.

The 752 Analyst

The danger of getting Recourse Debt wrong

The "Doomsday Simulation": Why Your Recourse Debt Allocations Might Fail under Audit.

The Sale of Interest: How to Calculate the Step-Up Without Blowing the Budget

The § 743(b) Calculator

The tedium of the step-up and the documentation

The Sale of Interest: How to Calculate the Step-Up Without Blowing the Budget

Stop Hard-Coding. Why "Target Capital" is the Only Safe Way to Handle Waterfalls

The Targeted Allocation Engine

The complexity of waterfalls vs. simple percentages

Stop Hard-Coding. Why "Target Capital" is the Only Safe Way to Handle Waterfalls

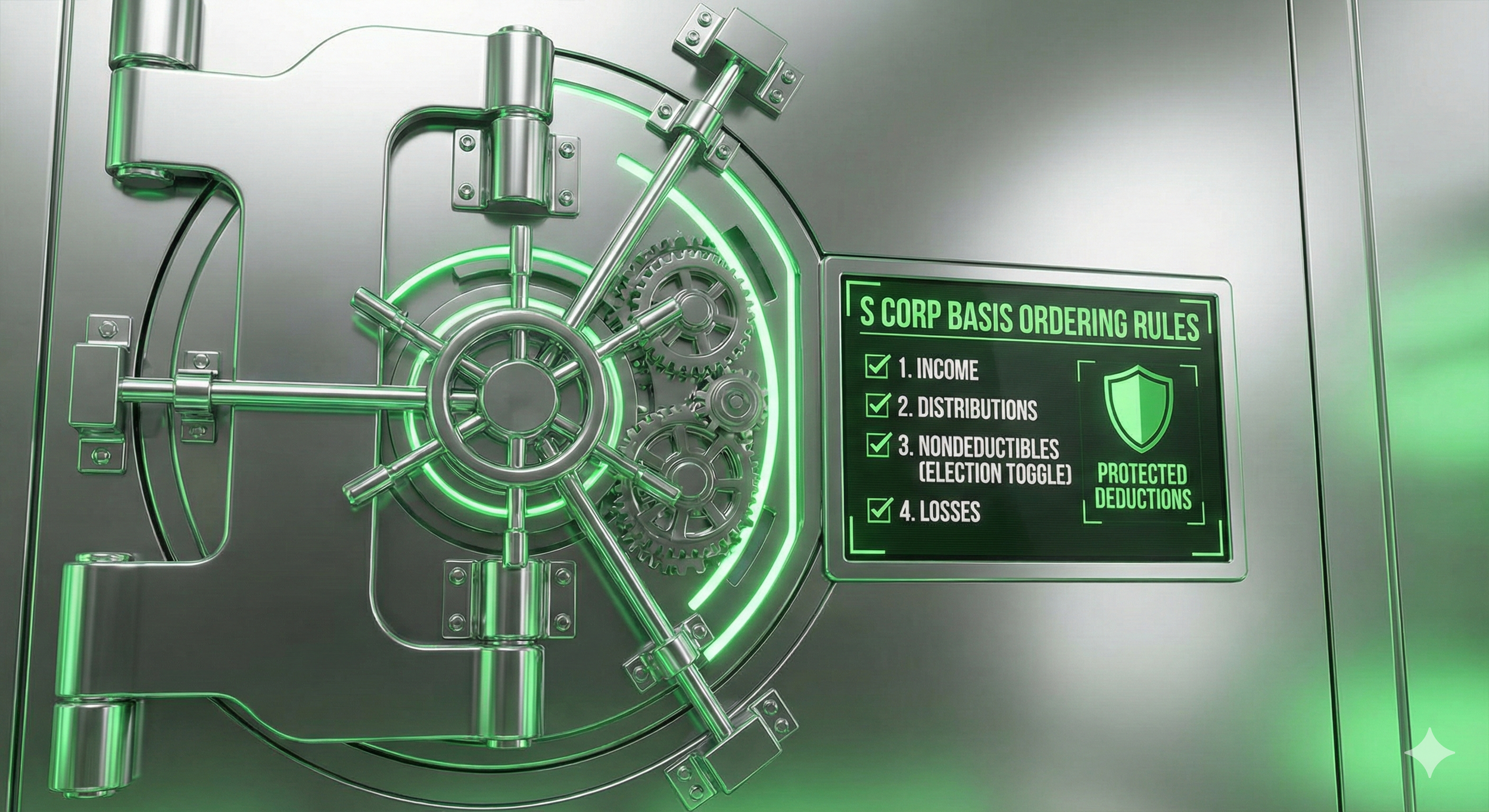

The Ordering Rule Trap: How One Toggle Can Save Your Client’s Deductions

The S Corp Basis Engine

The misunderstood ordering rules

The Ordering Rule Trap: How One Toggle Can Save Your Client’s Deductions